Home » Government Schemes

Category Archives: Government Schemes

Pradhan Mantri KIsan SAmman Nidhi 2019 Scheme: [6000 रु/year] प्रधानमंत्री किसान सम्मान निधि योजना

Pradhan Mantri KIsan SAmman Nidhi Scheme (प्रधानमंत्री किसान सम्मान निधि योजना) | PM – KISAN Scheme has been announced by the Indian Central Government. The Government launched this PM -KISAN Scheme for the Small & Marginals Framers. The Government with a view to augment the income of the Small and Marginal farmers has approved a Central Sector Scheme, namely, “Pradhan Mantri KIsan SAmman Nidhi (PM-KISAN) (प्रधानमंत्री किसान सम्मान निधि योजना)” in the current financial year. The Scheme takes effect from 01.12.2018 for transfer of benefit to eligible beneficiaries during this financial year 2018-19. With a view to providing income support to all Small and Marginal landholding farmer families having cultivable land, the Government has launched PM-KISAN. The scheme aims to supplement the financial needs of the farmers in procuring various inputs to ensure proper crop health and appropriate yields, commensurate with the anticipated farm income.

The objective of PM – KISAN: Pradhan Mantri KIsan SAmman Nidhi 2019 Scheme

The Central Government launched the Pradhan Mantri Kisan Samman Nidhi Scheme for the farmers who are in severe need of financial aids. These landholdings farmers would be provided with Rs 6000/- per year, per family payable in three separate equal installments. The Scheme is supposed to help farmers in their financial aids to support farming. Looking at the worsening condition of the farmers, this step has been taken to extend the help toward them. Earlier the pleas had been filed to for Agricultural Debt Waiver. But, Central Government denied the pleas saying that nullifying the debt will not solve the problems whereas a direct method of extending the help would be more efficient.

Under this scheme, the Central Government has adjoined certain Eligibility Criteria to separate out the offenders and repeaters. Only the Farmers who actually farm on their lands and are in dire need of financial support will be able to take advantage of this PM- KISAN Scheme.

The Benefits of Pradhan Mantri KIsan SAmman Nidhi Scheme 2019

The eligible Farmers would be able to take advantage of financial support. It is important to fulfill the Eligibility Criteria.

- Rs.6000 per annum per family payable in three equal installments, every four months directly to their bank accounts.

- The first installment to eligible beneficiaries during this financial year 2018-19 shall be for the period from 01 December 2018 to 31 March 2019.

- PM Kisan Samman Nidhi benefit to be provided to Landholder farmer families with total cultivable holding up to 2 hectares.

Definition of Eligible Farmers

A Small and Marginal landholder farmer family is defined as “a family comprising of husband, wife and minor children (up to age 18) who collectively own cultivable land up to 2 hectares as per land records of the concerned State/UT”. That means husband and wife and children will be considered as a unit. The existing land-ownership system will be used for identification of beneficiaries for the calculation of benefit. The names of those whose names will be found in the Land Records from 1st February 2019 will be entitled to the same.

A source attached to the Department of Agriculture said that former or presently constitutional post holder, current or former minister, mayor or district panchayat president, officers in central or state government and farmers who receive more than 10 thousand pensioners will not get the benefit. Professionals, doctors, engineers, CAs, architects, whoever farms, will not be considered entitled to this benefit.

Excluded Categories that cannot register for the Scheme are:

The following categories of beneficiaries of higher economic status shall not be eligible for the benefit under the scheme:

1. All Institutional Landholders; and

2. Farmer families in which one or more of its members belong to the following categories :

a) Former and present holders of constitutional posts

b) Former and present Ministers/ State Ministers and former/present Members of Lok Sabha/ Rajya Sabha/ State Legislative Assemblies/ State Legislative Councils, former and present Mayors of Municipal Corporations, former and present Chairpersons of District Panchayats.

c) All serving or retired officers and employees of Central/ State Government Ministries /Offices/Departments and its field units Central or State PSEs and Attached offices /Autonomous Institutions under Government as well as regular employees of the Local Bodies (Excluding Multi Tasking Staff / Class IV/Group D employees)

d) All superannuated/retired pensioners whose monthly pension is Rs.10,000/-or more(Excluding Multi Tasking Staff / Class IV/Group D employees) of above category (c))

e) All Persons who paid Income Tax in the last assessment year.

f) Professionals like Doctors, Engineers, Lawyers, Chartered Accountants, and Architects registered with Professional bodies and carrying out profession by undertaking practices.

Note: For the purpose of exclusion State/UT Government can certify the eligibility of the beneficiary based on self-declaration by the beneficiaries. In case the beneficiary is not available /does not reside in the village, State/UT Governments may consider certification based on the declaration by another adult member of his/her family. In case of the incorrect self-declaration, the beneficiary shall be liable for recovery of transferred financial benefit and other penal actions as per law.

Requirements

The farmers applying for the PM – KISAN Scheme must provide the following document as a Registered proof of

- Name

- Age

- Gender

- Category (SC/ST)

- Aadhaar Number

- Bank Account Number

- IFSC Code

- Land ownership

Note: In case of absence of Aadhaar, other identification documents issued by Central/State/UT Governments or their authorities like driving license, voters’ ID card, NREGA Job Card will be accepted for the first installment only. For beneficiaries in the States of Assam, Meghalaya, J&K, where Aadhaar number has not been issued to most of the citizens, Aadhaar number shall be collected for those beneficiaries where it is available.

Mobile number is not mandatory but can be provided when available to receive notifications on information related to sanction/transfer of benefit.

The validity of the list of beneficiaries for PM – KISAN

This list of beneficiaries prepared by States/Union Territories for transfer of the first installment shall be valid for one year. However, States/UTs can upload names of eligible beneficiaries who have been identified subsequently. States/UTs should also implement a mechanism to ensure revision of the name of the beneficiary list in case of mutation /changes in the land record after uploading list on the portal for updating the eligible beneficiary details for such lands. It should be noted that after 01.02.2019 benefit will be allowed to transferees only on succession due to death. For more details check the attached Pradhan Mantri KIsan SAmman Nidhi PDF file below.

Pradhan Mantri KIsan SAmman Nidhi PDF

Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) | 2018-19

The Pradhan Mantri Jeevan Jyoti Bima Yojana is a social security programme which was designed to provide life insurance coverage of Rs. 2, 00,000 (2 lakh) to all the subscribers on death due to any reason.

The scheme was introduced by the Honourable Prime Minister Narendra Modi along with two other social benefit insurance schemes Pradhan Mantri Suraksha Bima Yojana and Atal Pension Yojana. These schemes are aimed at the poor and middle-class sections of the society.

The Objective of Pradhan Mantri Jeevan Bima Yojana (PMJJBY) is to make the insurance policies affordable to the poor and middle-class sections of the society who are unable to avail life insurance policies (especially health / accidental) due to high insurance premiums. Also as India’s younger generation don’t have any pension to take care after retirement, securing financial future of their family in their absence will be of utmost important which would be taken care under PM Jeevan Jyoti Bima Yojana.

List of Banks Participating in Jeevan Jyoti Bima Yojana

- Canara bank

- State bank of India

- Bank of Maharashtra

- Industrial Development Bank of India (IDBI) bank

- Vijaya bank

- Union bank of India

- Jammu and Kashmir Bank

- Karnataka Bank

- Dena Bank

- The Madhya Bihar Gramin Bank (MBGB)

- Tamilnadu Mercantile Bank

- ICICI bank

- State bank of Travancore

- Punjab National Bank

- Punjab Gramin Bank

- Syndicate Bank

- Federal Bank

- Corporation Bank

- Jammu and Kashmir Bank

- HDFC Bank

- State Bank of Mysore

Click at the link to know the IFSC and MICR Code of any of these banks and their branches.

Role of the Participating Banks in Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

Apart from being the master account holders, banks have some other roles to play as well such as:

- The primary duty of the bank is to transfer the deducted amounts to the insurers.

- They will also have to look after the enrolment forms, authorisation of auto – debit, providing declaration-cum-consent form in the exact shape that they are supposed to be done.

Features of Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY)

- Rs.2 Lakhs i.e. after the death of the policy holder, this amount can be claimed by the nominee.

- Rs.330 only excluding the service tax. And this amount would be debited from bank account of the policy holder provided the person opts for long term option. In case long term option is not chosen then subscriber will have to opt every year.

- This policy offers one-year life insurance scheme renewable from year to year.

- Under this scheme the policy holder can exit the scheme at any time and join the same scheme in the future.

- Participatory banks will be the master policyholder of this scheme.

- Nominee can be declared at the time of buying the policy. And he/she can claim the benefits after unfortunate event of the death of the policy holder.

- The cover under PMJJBY is for death only and hence benefit will accrue only to the nominee.

- PMJJBY provides a convenient and a subscriber friendly insurance claim settlement process.

- In case an individual is having a life insurance policy anywhere, then such person can still enrol for PMJJBY and avail benefits.

- Individuals who fail to join the scheme in the initial year can join the scheme in subsequent years by annual premiums and submitting a self-certificate of good health.

- The premium amount towards PMJJBY is eligible for tax deduction under section 80C.

- Termination Condition of the Scheme

- If the person is above 55 years of age

- If the policy holder is covered through more than one bank account

- In case of insufficient balance in savings account to keep the insurance in force.

Eligibility Criteria under Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJBY)

- Under this scheme, the minimum age limit is 18 years and maximum age is 50 years.

- Cover would be available up to 55 years.

- Should have a savings bank account. In case of a person does not have a bank account, can open a zero-balance savings account under Pradhan Mantri Jan Dhan Yojana (PMJDY).

Subscription Procedure of Pradhan Mantri Jan Dhan Yojana (PMJDY)

- Open a savings bank account with any of the participating bank

- Fill the application form provided from the bank

- One can also provide a copy of Aadhaar Card as the primary Know Your Customer (KYC) document.

- One can subscribe to this scheme every year in the month of June or they can choose a long – term subscription period where your account will be auto – debited every year.

Difference between PMSBY and PMJJBY

| Feature | Pradhan Mantri Suraksha Bima Yojana (PMSBY) | Pradhan Mantri Jeevan Jyoti Bima Yojana (PMJJBY) |

| Age limit | 18 – 70 years | 18 – 50 years |

| Assured Sum | 2,00,000 | 2,00,000 |

| Premium (Annual) | Rs. 12 | Rs. 330 |

| Cover ceasing age | 70 | 55 |

| Death Benefit (Not by accident) | NIL | 2,00,000 |

| Death Benefit (By accident) | 2,00,000 | 2,00,000 |

| Disability of both eye, both hands, both legs or one eye and one limb | 2,00,000 | NIL |

| Disability of one eye or one limb | 1,00,000 | NIL |

| Maximum Cover | 2,00,000 (From any one of bank account) | 2,00,000 (From any one of bank account) |

| Risk Period | 1st June to 31st May every year on deduction of premium | 1st June to 31st every year on deduction of premium |

| Mode of Payment | Auto debit from bank account | Auto debit from bank account |

Highlights of the Pradhan Mantri Jeevan Jyoti Bima Yojana

- Eligibility: Available to people in the age group of 18 to 50 and having a bank account. People who join the scheme before completing 50 years can, however, continue to have the risk of life cover up to the age of 55 years subject to payment of premium.

- Premium: Rs.330 per annum. It will be auto-debited in one instalment.

- Risk Coverage: Rs.2 Lakh in case of death for any reason.

- Who Will Implement this Scheme? All the banks and insurance companies who are willing to participate in PMJJBY.

Senior Citizen Savings Scheme | 2018-19

In every society, senior citizens are always given the special place and consider them as the head of the family. In India, any people who have attained the age of sixty years or above are considered as senior citizens.

And in order to acknowledge their contributions and help them retiring gracefully, Government of India honours them by offering them wide range of attractive programs and facilities. The ‘Senior Citizen Savings Scheme’ (SCSS) is one of them.

Senior Citizen Savings Scheme (SCSS) is a government program for the senior citizens (who are above the age of 60 years) to provide them additional retirement benefits while availing day to day cash requirements.

This scheme is considered to be one of the safest investment schemes as it is backed by the government. These schemes are available through banks and post offices which are associated with SCSS. The SCSS account can be elongated for 5 years and upon maturity can be extended for 3 more years. Under this scheme, depositors are permitted to make one deposit into this account.

Senior Citizen Savings Scheme is a well – made, shielded and a highly targeted savings scheme among the senior citizens of India.

Interest Rates for Senior Citizen Saving Scheme

Below is the table of interest rate for the first quarter of Financial Year 2017 – 18 i.e. April 17 to June 17.

| Investment Option | Rate of Interest for Quarter 1: April 17 to June 17 |

| Senior Citizens Savings Scheme (SCSS) | 8.40% |

Benefits under Senior Citizen Savings Scheme

SCSS is a very beneficial product for senior citizen in India as it offers one of the best interest rate among the other government programs along with customised facilities in order to fulfil every requirement of the senior citizens.

Read below to know some of the benefits of Senior Citizen Savings Scheme (SCSS)

- This scheme offers a hassle free processing where an interested applicant have to just fill up an application form at their nearest post office or a local bank along with required documents and initial deposits in order to get the account opened.

- This scheme is the most reliable scheme as it is backed by the government itself; hence it comes with all the protection and assertion associated with the government schemes.

- It offers the option of handling multiple accounts at the same time which could be either operated as singly or jointly with the subscriber’s spouse.

- This scheme is offering a very attractive interest rate which is of 8.6% per annum.

- ‘Senior Citizen Savings Scheme’ encourages senior citizens to save as it is a medium for a long term investment product as this account offers 5 years maturity term period and can be further extended for 3 more years.

- This investment scheme is eligible for a tax rebate of under section 80 C, of the Income Tax Act, 1961. Hence, it is extremely helpful in saving tax.

- This scheme is flexible in investment amount as in this scheme one can invest any amount in multiples of Rs. 1000 up to the maximum cap of 15 lakhs. However, this can be done only once. And the amount plus interest can be directly credited into the depositor’s savings bank account held with the bank branch or to the linked Post Office Savings account.

- The subscribers of this scheme can prematurely withdraw from their SCSS scheme. However they would be subjected to the penalty of 1.5% of the funds till 2nd year of completion and 1 % post 2 years till the 5th year.

- As this scheme is designed for the senior citizens, the process of enrollment has been kept simple and hassle free. The only documents which are required are age – cum ID proof, it could be Passport, Voter’s ID, Birth Certificate, Aadhaar Card, PAN card, Senior Citizens Card etc.

Eligibility Criteria for Senior Citizen Savings Scheme

As the name suggest, this scheme is only for the senior citizens of the country i.e. individuals aged 60 years or above are eligible to subscribe to this scheme.

However, any individual who is not 60 years yet, but have attained 55 years of age and have taken VRS (Voluntary Retirement Scheme), can also apply for this scheme and the account should be open within 1 month of the receipt of retirement benefits.

At the same time, any retired defence official irrespective of above mentioned age limits are eligible to subscribe to this scheme, however, they are subjected to other terms and conditions.

Hindu Undivided Families (HUF) or Non Resident of India (NRIs) are not eligible for the scheme.

How to Open a SCSS Account

Interested people can open a SCSS account by visiting a local bank or by visiting nearest post office

Opening a SCSS account by visiting Post Office

As we know Indian Postal System still has a reach in the remotest India. Hence most of the government sponsored schemes are available in Indian Post Office. The SCSS is hence also offered at all the Post Offices of India. And this scheme has indeed flourished at post offices as the non – urbanized population can also easily access to this scheme at the post office

Opening a SCSS account by visiting an authorized Bank

There is a selected public / private sector bank which offers SCSS account. The reason this scheme is offered through a bank as well because banks today facilitates people with round the clock service and they have branches in most of the rural areas.

Read below to know the list of banks which offers SCSS account:

- Allahabad Bank

- Andhra bank

- State Bank of India

- State Bank of Mysore

- State Bank of Bikaner and Jaipur

- State Bank of Patiala

- State Bank of Travancore

- State Bank of Hyderabad

- Bank of Maharashtra

- Bank of Baroda

- Bank of India

- Corporation Bank

- Canara Bank

- Central Bank of India

- Dena Bank

- Syndicate Bank

- UCO Bank

- Union Bank of India

- Vijaya Bank

- IDBI Bank

- Indian Bank

- Indian Overseas Bank

- Punjab National Bank

- United Bank of India

FAQs

PMAY | 2018 | Application Process | Pradhan Mantri Awas Yojana

Previously called “Housing for All”, Prime Minister Narendra Modi launched Pradhan Mantri Awas Yojana (PMAY) in 2015 to provide a place to reside for millions of urban poor. The Government has already identified over 2,508 cities and towns across 26 states in the country with an aim to build over 2 million houses.

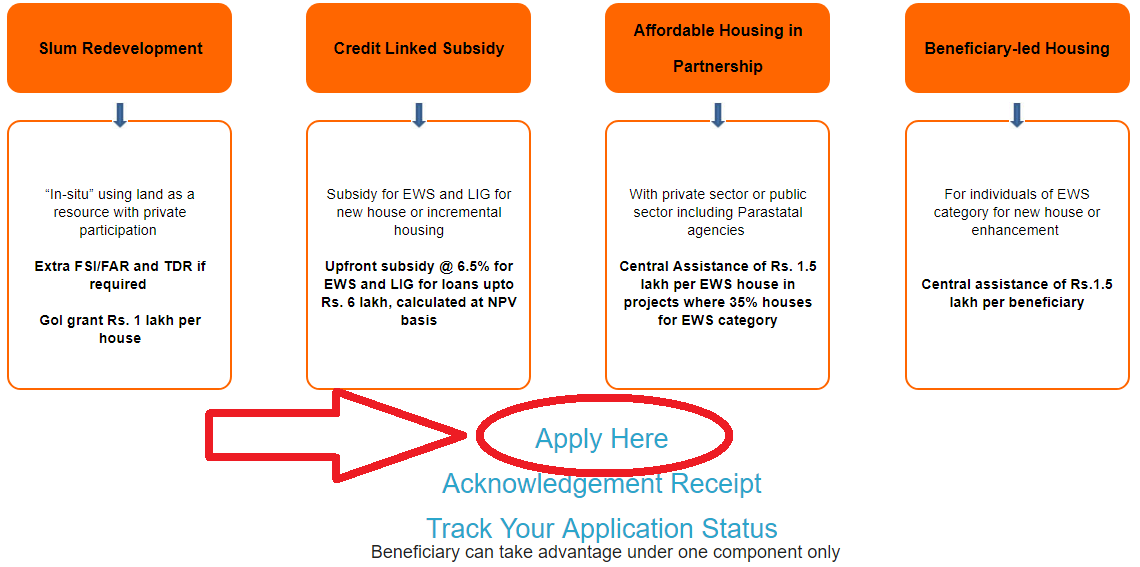

Pradhan Mantri Awas Yojana (PMAY) can be applied by two categories

- MIG, LIG and EWS (Other 3 Components) – The economically weaker sections like MIG, LIG and EWS are considered as beneficiaries under the Housing for All by 2022.

- Middle Income Group (MIG) – annual income between Rs. 6 lakh and Rs. 18 lakh.

- Lower Income Group (LIG) – annual income is between Rs.3 lakh and Rs.6 lakh.

- Economically Weaker Section (EWS) – annual income stands at Rs. 3 lakh.

- Slum Dwellers – Slum areas are poorly built residences where 60 to 70 households or approximately 300 people stay. These areas are unhygienic as they lack proper sanitation facility, proper infrastructure and drinking water. People living in these people can apply for the Housing for All by 2022 Scheme under the Pradhan Mantri Awas Yojana.

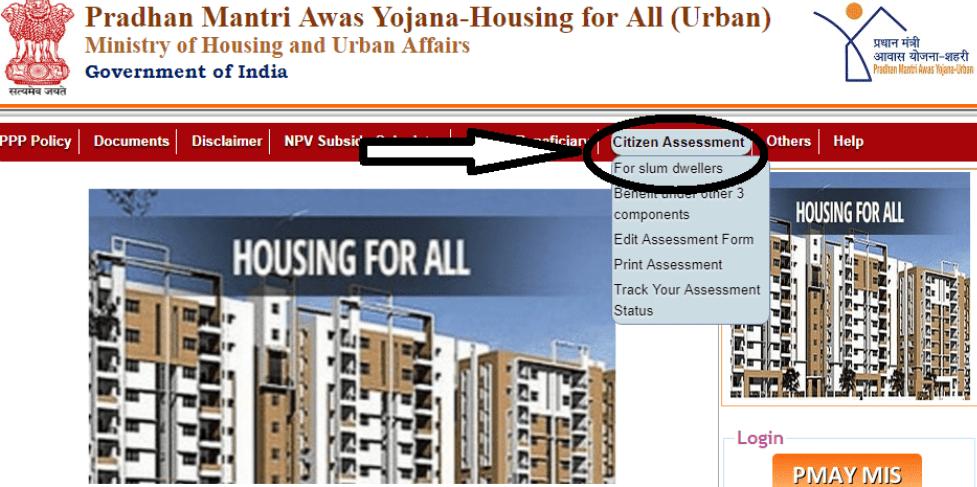

Applying for PMAY under Other 3 Components Online

- Visit the official PMAY website http://pmaymis.gov.in/

- Click on “Citizen Assessment” and select “Benefit under Other 3 Components” from the options.

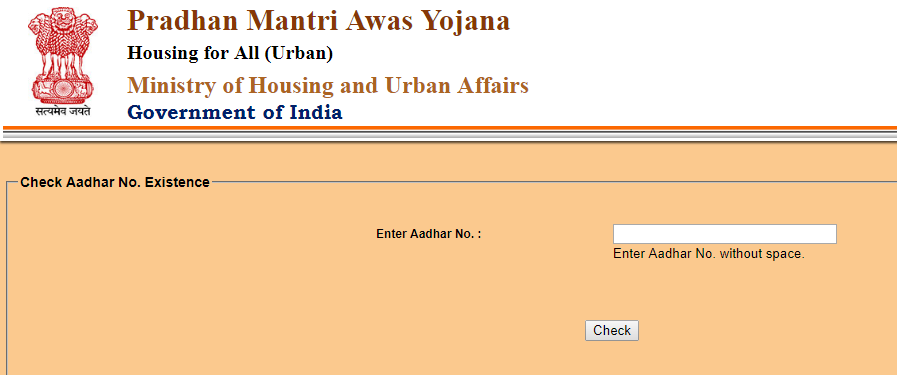

PMAY Citizen Assessment Official website - Enter your Aadhaar number and click submit

PMAY Aadhaar Form - If the information’s you provided is correct, it will direct you to the next page and you will be asked to provide information’s which include name, income, no. Of family members, residential address, contact number, age of the head of the family, religion, caste.

- Once all the information is provided, scroll down, type the captcha code in the box and click submit.

Applying for PMAY by the Slum Dwellers

- Log on to the official website of PMAY http://pmaymis.gov.in/

- Click on the “Citizen Assessment” and select “For Slum Dwellers” from the options.

PMAY Slum Dweller Official website - Enter your Aadhaar number and click on submit.

PMAY Aadhaar Form - If the information’s you provided is correct, it will direct you to the next page and you will be asked to provide information’s which include name, income, no. Of family members, residential address, contact number, age of the head of the family, religion, caste.

- Once all the information is provided, scroll down, type the captcha code in the box and click submit.

Online Application for PMAY through Citizen Service Centre (CSC)

Follow the below steps to apply for PMAY online:

- Visit the official website of Pradhan Mantri Awas Yojana (PMAY) of Common Service Centers (CSC) https://registration.csc.gov.in/pmay/

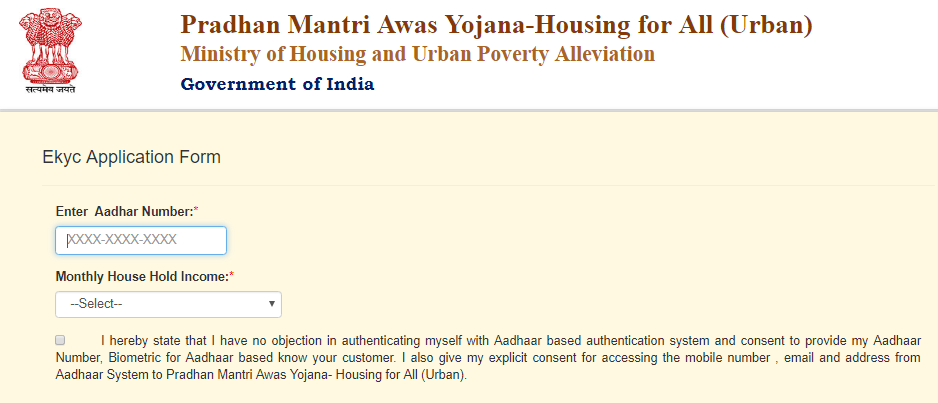

- Click on the “Apply Here” link or directly visit https://registration.csc.gov.in/pmay/RegAuth.aspx

PMAY Applying procedure Official Website - On this page, enter your Aadhaar number and select the monthly household income, check the declaration box and click “Next” for the next step.

PMAY Aadhaar Verification - In this step, you will be asked to select a verification method, choose one from the Iris (Eye scan), Fingerprint or One Time Password (OTP).

- Now, check the declaration check box and click on “Generate OTP”. After receiving OTP on the Aadhaar registered mobile number, enter the OTP and click “Validate OTP” button.

- An application form will be provided on the next page. Fill the required details properly and submit it.

- Next Screen will show an application number or assessment ID which can be used to check the status of PMAY application

Note: Use IE8 or Mozilla Firefox as Google Chrome or Microsoft Edge Browser are not supported.

You can check the status of your application here http://pmaymis.gov.in/Track_Application_Status.aspx by entering your name, Father’s name and ID Type or by Assessment ID.

Pradhan Mantri Sahaj Bijli Har Ghar Yojana (PMSBHGY)

Recently, Prime Minister Shri Narender Modi launched Pradhan Mantri Sahaj Bijli Har Ghar Yojana (PMSBHGY) which aims at providing ‘last mile electricity connectivity to all rural and urban households’.

The main purpose of the scheme is to provide energy access to all households in the country in rural as well as urban areas to meet universal household electrification in the country.

Use of electricity improves quality of life and it plays an important component for the human development and economic growth of the country. First of all, access to electricity decline the use of kerosene which plays and important fuel in the households particularly in the rural areas which results in hazardous emissions thereby access to electricity will save people from health hazards. Also, it is the central to the ability of almost all developed societies to function and enjoy the modern amenities available to them.

According to the Ministry of Power,

Beneficiaries of Pradhan Mantri Sahaj Bijli Har Ghar Yojana

Under the Sahaj Bijli Har Ghar Yojana, the beneficiaries for free electricity will identify by using Socio Economic and Caste Census (SECC) 2011 data. Despite that, if any of the household is not covered under SECC, they can also avail the scheme by paying the nominal charges of Rs. 500 which will recover by DISCOM in 10 installments through electricity bill.

For houses located in remote and inaccessible areas where it is not viable to extend grid lines, solar power packs of 200 to 300 Watt and battery back with 5 LED light. 1 DC Fan, 1 DC power plug would provide along with Repair and Maintenance (R and M) facility for 5 years.

Implementation of Pradhan Mantri Sahaj Bijli Har Ghar Yojana

The government have decided to use Mobile app in order to conduct household survey for fast and easy implementation of the scheme. Government will do the identification of the beneficiaries by using Socio Economic and Caste Census (SECC) 2011 data and their application for electricity connection along with their photograph and identity proof and register them on the spot. The Gram Panchayat / Public institutions in the rural areas may be authorized to collect application forms along with complete documentation, distribute bills and collect revenue in consultation with the Panchayat Raj Institutions and Urban Local Bodies.

Note: [The Rural Electrification Corporation Limited (RECL) will remain the nodal agency for the operations for the scheme throughout the country].

Expected outcome of the scheme

The expected outcome of the scheme is as follows:

(a) Environmental up gradation by substitution of Kerosene for lighting purposes

(b) Improvement education services

(c) Better health services

(d) Enhanced connectivity through radio, television, mobiles, etc.

(e) Increased economic activities and jobs

(f) Improved quality of life especially for women

The Government have asked the States and Union Territories to complete the household electrification work by the 31st of December 2018.

FAQs

So wide multi – media campaign would be undertaken to make people aware of all aspects the Scheme. The DISCOM officials would also organize camps in rural areas for creating awareness about electricity as well as Saubhagya. School teachers, Gram Panchayat members, local literate / educated youth would also be associated in the awareness campaign.